— From Rothbard at 100: A Tribute and Assessment, Stephan Kinsella and Hans-Hermann Hoppe, eds. (Houston: Papinian Press and Property and Freedom Society, 2026) —

5

Three Channels of Asset Inflation

Murray Rothbard has made numerous important contributions to all major fields of economics, and he also excelled as a historian and political philosopher. The main focus of his work was the comparative study of government interventionism, or statism, as opposed to the workings of a free society. Here he underscored again and again the crucial importance of monetary interventionism. A good number of his most widely-read books and pamphlets have dealt in detail with fractional-reserve banking, central banking, and fiat money.

One related area which he had somewhat neglected because in his lifetime it did not play quite the same paramount role that it has come to play in the past thirty years, is the study of financial markets. If he had lived longer, he surely would have set out to analyze the nature, causes, and consequences of financial exchanges. He would have brought them into the purview of the Austrian approach that he had inherited from Menger and Mises, and which he himself had developed in so many other areas.

And so it came that many of my own writings of the past twenty years or so have dealt with the issues of financial economics, as this field of inquiry is today often called. In 2013, I published a German-language book dealing with the political economy of finance, which was published under a somewhat misleading title, Krise der Inflationskultur (Crisis of the Inflation Culture). An English translation was in preparation, but never released due to my own reticence. My plan has been to incorporate various new elements into the English edition, but several of these elements have still not been fully worked out. One exception is the present text, which represents an updated version of chapter VIII of that book. I therefore offer it to the memory of the great Murray Rothbard, and I thank my friends Stephan Kinsella and Hans-Hermann Hoppe for assisting with the translation.

* * *

In a fiat-money system, wealth tends to grow faster than incomes. In more technical terms, the aggregate market capitalization of all assets, including most notably financial securities and real estate, tends to grow faster than the money revenues earned on factor markets and consumer goods markets. This tendency is sometimes called asset inflation. It can be measured in various ways.

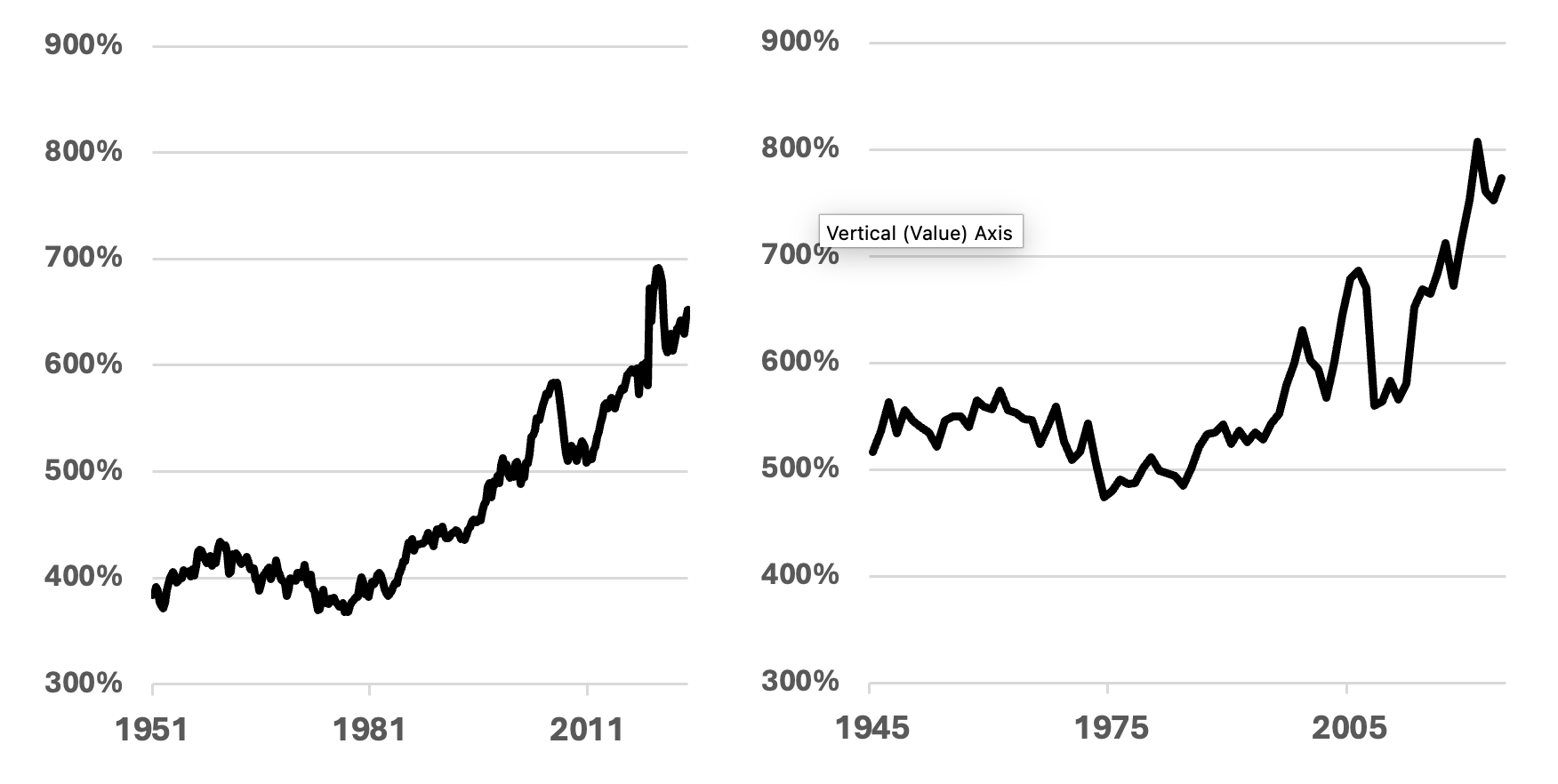

The left panel on Figure 1, below, features the value of all assets held by US households relative to GDP from 1951 to 2025. The right panel features the ratio of the net worth of US households relative to their disposable personal income from 1945 through 2024. Both metrics show that during the first three decades after WWII, the wealth-to-income ratio was more or less stagnant. After the collapse of the Bretton Woods System, the ratio started to increase, very slowly at first and then strongly as from the mid-1980s. This tendency was interrupted here and there by financial crises. But the general trend is intact to the present day.

Figure 1: Asset Growth in the USA

Source: FRED St. Louis: GDP, TABSHNO, A792RC0A052NBEA, and HNONWRA027N

Asset inflation has not received the attention it deserves, neither in the mainstream literature, nor among Austrian economists. Mainstream authors typically believe that asset inflation has nothing to do with monetary interventionism.2 Austrians are in a much better position. Nourished by the writings of Mises and Rothbard, they know that monetary policy affects the price structure (not just the general price level) and may also entail significant disequilibria, both in the real and the financial sectors of the economy. Accordingly, Philipp Bagus and Brendan Brown have interpreted asset inflation as a prolonged boom, fueled by below-equilibrium interest rates out of the printing press. Zukauskas and Hülsmann have underscored the influence of the quality of money and of Cantillon effects.3 In the present contribution, I will largely neglect these factors, important though they are, and instead focus on three other channels: a collateral channel, a price-inflation channel, and a moral-hazard channel.

Banking-Style Money Creation and the Asset Markets

Present-day fiat-money systems would entail a relative growth in the financial and real estate markets (as compared to the real economy) even if there were no price-level increases and no increases of the money stock. The reason is that virtually all units of money are supplied to the market in the form of loans. Ludwig von Mises called this the “banking-style” (bankmäßige) creation of money.4 The ex nihilo creation of new units of money then occurs in the context of a corresponding ex nihilo creation of loans (“credit expansion”). And the continued circulation of all units of money is due to the fact that the corresponding loans have not yet expired. Money and credit are tied at the hip.

It does not necessarily have to be that way, and historically it has not. Until the 19th century, various note-issuing fractional-reserve banks have issued banknotes in a non-banking-style way. Instead of lending the notes, they occasionally spent them outright on wages and supplies, and sometimes gifted them to political authorities.5 It is clear that this practice is fraught with great dangers for a fractional-reserve bank. After all, the bank has to stand ready to redeem its notes and deposits into base money. By lending its notes and deposits, on the other hand, it obtains a claim on base-money payments at some point in the near future. This, we may surmise, is why the practice of banking-style money creation has become universal. Today, money is not given away, but lent out. The overall quantity of money in circulation is tied up with a corresponding volume of loans.6

Loans are usually collateralized. Real estate loans to private households are secured by a mortgage on the houses and land purchased. Medium to long-term corporate financing is also often secured by the real estate of the borrowing firms. Securities such as government bonds, treasury bonds, shares and bills of exchange often serve the same purpose. Before the 2008 crisis, commercial banks also lent each other unsecured money—in the so-called interbank market—but this custom has come to a standstill.7 Today, they usually only lend to each other if securities or gold are deposited as collateral. The same procedure is followed for central bank loans to commercial banks. The technical details are sometimes quite different, but the principles are basically the same.

Real estate is quite suitable for loan collateralization in the context of mortgage loans because it typically carries a relatively low price-risk. Nor can it simply be stolen and taken out of the country.8 Financial securities can be much more suitable for collateralizing loans, because they always can be managed and resold relatively cheaply, even for very large sums. But trouble may spring from counterparty risks and lacking liquidity. This is why, among all financial securities, IOUs on a national government (Treasury Bills, government bonds, and similar) are eminently suitable as collateral for all other credit transactions.

Most other assets cannot boast comparable benefits.9 This applies in particular to entrepreneurial business assets. Plants, machines, and tools are often not generally usable, but are tailored to a specific product group. There is no significant secondary market for such goods. Even if their purchase may have cost many millions and perhaps billions of dollars, they can sometimes only be sold at scrap value, even when new. Such goods are therefore unsuitable as collateral.

To sum up, the production of money by credit increases the demand for real estate and financial securities beyond the level that would occur in a natural monetary order.10 These goods are valued not only because of their direct services, but also because they are particularly well suited to serve as collateral. Certainly, this “collateral-quality” demand would also play a certain role in a natural monetary order, because here too there would be loans that would have to be collateralized. But in a fiat money system, in which money is created by credit, it is multiplied.

As a result, the market prices of real estate and securities are higher in a fiat money system than in a natural monetary order. Real estate prices not only reflect the use-value of the properties in question for their owners; securities prices are not only determined by their risk and expected return.11 In both cases, the prices for such assets also include a premium that reflects their value in serving as collateral for loan. The return on investment in these goods is correspondingly lower. The purchase of real estate and securities tends to generate lower returns (interest or dividends) than the purchase of industrial production factors.

These tendencies are further reinforced by the fact that the demand for these assets as collateral increases their marketability or liquidity. It becomes easier to find buyers quickly and at low cost and to sell the assets without significant discounts. Because such liquidity is tantamount to a higher quality of assets, or a lower risk for the investor, the demand for these assets increases even further.

Notice that this does not merely concern the demand side. It also concerns the supply side of the market for any durable good, and in particular for real estate or financial securities. The reason is that, on such markets, both demand and supply are largely determined by the same factors.

Things are different on most other markets. Most products that emerge under the division of labor have buyers and sellers with distinctly different motivations. The producers are usually not interested in owning or using these goods themselves; they primarily want to earn a monetary income. For example, a car manufacturer typically wants to sell all of its vehicles; he has no need for a personal fleet of several million cars.

However, once durable assets have been sold by their producer, the new owners are typically motivated by the same factors that drive the choices of all other people who may wish to acquire them in the future. In other words, the demand side of the market is then determined by the same factors as the supply side. If the demand for real estates and financial securities increases because they may also serve as collateral, then this affects not only the interested buyers (the demand via exchange), but also the current owners (the reservation demand). Both groups then appreciate the asset more than before. The potential buyer is willing to pay a higher price, but the seller is also asking for a higher price, and for the exact same reasons.12

Let us summarize our findings. The production of money through credit increases the demand for real estate and financial securities because these goods are well suited to serve as loan collateral. Their market prices therefore tend to be higher in a fiat money system with credit money creation than in a natural monetary order; a capital investment in these goods generates correspondingly lower returns.

Now, where do the additional sums of money that are exchanged on the asset markets come from? After all, if higher prices are paid for real estate and securities, the money has to come from somewhere. If the money stock does not increase, the premium for real estate and securities can only be paid by corresponding cuts somewhere else. Accordingly, either cash balances must shrink, or consumer spending must fall, or the purchase of factors of production must decline; or some combination thereof. This implies that the money values of all these other goods will tend to fall relative to the money values of assets. This would even hold true in the extreme case in which the entire collateral premium were to be fully paid out of existing cash balances (that is, without spending cuts elsewhere); for then the aggregate money values of consumer goods and of factors of production would not shrink in absolute money terms, but they would shrink relative to asset prices. In all other cases, in which there would be spending cuts elsewhere, this relative shift in money values would be even stronger.

This shift implies that the aggregate money incomes out of non-financial activities become less important as compared to financial activities. Moreover, and most importantly, it also implies that the aggregate money values of all incomes tend to shrink relative to the aggregate money values of all wealth. Statistically, this shows up in an increased wealth-to-GDP ratio. Non-financial activities (the large bulk of the economy) will be less well remunerated if less money is spent on factors of production and on consumers’ goods. Some bankers, insurance agents, and fund managers will earn higher incomes, but these increases tend to be marginal from an overall point of view. But if aggregate incomes diminish relative to aggregate wealth, the implication is that it takes more work to accumulate any given level of wealth. People have to work longer years, or longer hours, or they have to save more, in order to acquire any given amount of real estate and financial securities.13

Notice that the collateral premium, and its implications for the income-wealth ratio, is independent of the concrete objectives of monetary policy. Whether the central bank targets the stabilization of a consumer-price index (CPI), or any more comprehensive target, such as the GDP deflator, or a broader index including asset prices, the basic mechanism that we just discussed does not change. It would not change even if the central bank set out to freeze the overall money stock at its existing level. Whenever new money units come into circulation through new credits, asset prices tend to rise relative to the prices of consumer goods and of factors of production. As a further consequence, the aggregate money value of assets increases relative to aggregate income.

As we shall see in what follows, this tendency is greatly reinforced by a policy of creeping price inflation. All central banks of our time inflate the money supply to such an extent that the CPI constantly rises at low single-digit rates (creeping price-inflation), and this stimulates financial leverage and the credit market. However, in order to see where exactly monetary interventionism comes into play, we need to consider the possibility that the CPI could rise even without any government intervention whatsoever.

Under a completely free market for money, it would indeed be conceivable that abundant silver and gold mines were discovered, such that the annual output of gold and silver would outpace the output in all other industries. Then the CPI could rise over prolonged periods of time. This scenario is of course very unlikely, for reasons which we will discuss below, but it is a possible scenario. Accordingly, in what follows, we will first consider this improbable scenario and only then move on to the more realistic assumptions. This mental experiment will allow us to isolate the specific effects that arise from policy-induced increases in the money supply.

Asset Markets Under Creeping Price Inflation in a Natural Monetary Order

Permanent low-level price inflation brings about an over-proportional growth in asset markets, regardless of the specific cause of price inflation. One basic reason is that, under creeping price inflation, it is not advisable to hold any savings in cash.

Those who hold any savings in the form of cash balances lose the purchasing power that they have saved in the past. Savers then have by and large two options. Either they do not save at all, but spend their cash balances on consumers’ goods. Or they use these cash balances to purchase real estate and financial securities, that is, assets with a built-in protection against price-inflation. Indeed, the monetary value of these goods increases along with the ambient price inflation, and some of them also yield revenue and thereby compensate (at least partially) for the price inflation. Creeping inflation therefore stimulates investments in interest-bearing savings accounts, life insurance policies, and so on.14 In other words, the supply of savings on the market for loanable funds (on the credit market) increases.

A similar expansion is also occurring on the demand side of that market, albeit for a different reason. If the price level is relentlessly rising, and if further increases are expected in the future, then all market participants have a strong incentive to finance their investments with loans, rather than with their own money. The reason is that in a price-inflationary environment, debt offers the opportunity to increase and multiply the return on equity (ROE). Economists call this the leverage effect. Firms take advantage of this effect just as much as private and public households.

In an environment of creeping price inflation, firms can expect to be able to sell their products at higher unit prices in the future, with unchanged or even increasing sales volumes in real terms. This creates an almost irresistible incentive to fund any new investments with a fixed-interest-rate loan. As long as the borrowing costs are lower than the returns on these investments, a higher return on equity can be achieved through acquiring debt, through borrowing.

Since this is a very central mechanism, we will illustrate it with a numerical example. Suppose a company buys 50 million euros worth of factor services every year, with the help of which it creates products whose subsequent sale leads to an expected gross revenue of 52.5 million euros. The company thus achieves a net revenue of 2.5 million euros, corresponding to a of 5 percent operational return on investment (ROI). If credit market costs were about as high (say, interest and principal payments would amount to 5 percent of the loan), then the company would have no particular extra incentive to incur debt.

Now suppose that the discovery of a very productive silver mine brings large amounts of additional silver money to the market. The company therefore expects to achieve higher unit prices for its products in the future and considers expanding its operations. Henceforth it plans to purchase every year factor services that are worth 100 million euros, and annual sales are expected to increase to 110 million euros. This would mean a gross revenue of 10 million euros, and the operational ROI would thus rise to 10 percent.

It can finance the investment sum of 100 million euros through any mixture of equity capital and loans. If it is still able to borrow at a fixed interest rate of 5 percent, the respective mix of equity and loans has a major influence on the net income or on the return on equity. Consider four hypothetical scenarios, which we will summarize in the table below.

| I | II | III | IV | |

| Gross revenue | 110M€ | 110M€ | 110M€ | 110M€ |

| Business spending | 100M€ | 100M€ | 100M€ | 100M€ |

| Operational net revenue | 10M€ | 10M€ | 10M€ | 10M€ |

| Operational ROI | 10% | 10% | 10% | 10% |

| Equity capital | 100M€ | 40M€ | 10M€ | 1M€ |

| Debt | 0 | 60M€ | 90M€ | 99M€ |

| Debt costs | 5% | 5% | 5% | 5% |

| Debt service | 0 | 3M€ | 4,5M€ | 5M€ |

| Net revenue after debt service | 10M€ | 7M€ | 5,5M€ | 5M€ |

| ROE | 10% | 17,5% | 55% | 500% |

Figure 2

The leverage effect

If the annual business spending is funded exclusively by equity capital (Scenario I), the return on equity is exactly equal to the operational ROI, namely 10 percent. Debt financing improves this outcome, because the cost of borrowing is now suddenly lower than the operational ROI. The higher the debt ratio, the stronger the return on equity (ROE). In scenario II, 60 million euros are financed by debt and 40 million by equity. As a result, the net revenue drops to 7 million euros (because 3 million are needed for servicing the debt, including interest and repayment), but the ROE increases, because those 7 million are the remuneration of an equity of only 40 million euros. In scenario III, the leverage ratio is even higher, and the ROE increases accordingly. Finally, scenario IV shows the seemingly extreme case in which only 1 million euros of equity are used, while the remaining investment sum of 99 million euros is financed by loan. In this case, the company’s net revenue after debt service drops to just over 5 million euros; but this sum remunerates, as previously noted, an equity of only 1 million. In other words, the ROE in this case is 500 percent!

As long as the cost of borrowing is lower than the operational return of the company, a growing leverage ratio leads to growing ROEs. However, this leverage effect is not linear, but exponential. A steady increase in the leverage ratio leads to ever greater increases in the ROE.

The leverage effect explains why business owners (as well as financial firms) may have an incentive to fund their business spending out of loans. But the same thing may be said about private and public households. In a price-inflationary environment, it is to be expected that incomes (private) and tax revenues (government) will rise sooner or later. If the loan costs remain unchanged (fixed interest rate), there is an incentive to take on more debt because these costs can be expected to decline relative to income.

Private households typically use loans to purchase durable assets such as real estate or the shares of companies listed on a stock exchange. They therefore stand to benefit in a double way from price inflation: because the loan costs are bound to decrease relative to income, and also because the monetary value of their assets is also bound to increase with the general price inflation.

Public households (municipal, state, and federal governments) are special debtors with strong incentives to take on debt. Under permanent price inflation, they can expect tax payments to grow, along with the growing incomes of the citizens and with the growing monetary values of private assets. If price inflation coincides with progressive income tax rates, government revenue typically increases at a higher rate than the price-inflation rate.

Under permanent price inflation, there are therefore are strong incentives for financial leverage in all sectors of the economy. The supply of promises to pay (the demand for loans) is therefore bound to be growing.

All in all, then, the situation is as follows. Creeping price inflation entails growing credit markets. On the one hand, the demand for interest-bearing promises to pay (the supply of loans) is increasing. On the other hand, the supply of promises to pay (the demand for loans) is also increasing.

Similarly, real estate markets are growing under creeping price inflation, too. On the one hand, some of the previously hoarded cash balances are now used to buy real estate; on the other hand, there is an increase in credit-financed purchases by companies and households who want to take advantage of the leverage effect.

The price level of assets will therefore tend to rise. In the case of real estate, this is obvious. In the case of securities, this tendency is less obvious, but ultimately just as apparent. It is true that there is a simultaneous expansion of supply and demand, and these direct influences do not provide a clear direction for the development of the price level of securities. But indirectly, the influence of the demand for promises to pay tends to be preponderant, for three reasons. Firstly, the higher volume of credit also requires more extensive collateral, and thus the demand for real estate and especially the demand for debt securities increases. Secondly, the liquidity of securities is increasing due to the general growth of the credit market. Thirdly, credit scores are rising along with the rising prices of real-estate (collateral values).

The growth of the asset markets due to price inflation may be accompanied by an overall increase in the volume of savings. Some savers will wish to offset the expected future rise of the price level by a higher volume of savings. Other will save less, as a consequence of the incentives to buy short-lived consumer goods. In any case, creeping price inflation entails less savings in cash and thereby deteriorates the material conditions of life for the financially illiterate population. Although the banking industry is growing, it is doing so at the expense of cash balances, and some previously hoarded funds are no longer saved but spent.

* * *

The foregoing considerations concern creeping price inflation in general, that is, irrespective of whether it results from monetary interventionism or occurs in a purely free-market setting. It also does not matter whether the new money units are brought into circulation via new credits creation, or by outright payments, or through gifts. Creeping price inflation always and everywhere provides a shot into the arm of the credit market and thereby entails a tendency for the prices of real estate and financial assets to rise.

However, within the context of a natural monetary order, these tendencies are strongly limited, for six major reasons.

First, natural money production is costly. In the few historical periods when the discovery of abundant silver and gold mines entailed a significant increase of the overall money stock, this increase was always moderate in comparison to fiat-money systems. The resulting price inflation was kept within very narrow limits.

Second, in a natural monetary order, strong increases in the money stock are temporary and price-level increases are therefore temporary, too.

Third, a higher level of indebtedness means a greater vulnerability of the debtor. An entrepreneur who operates with ten percent equity exposes himself to a very high risk of insolvency. Equity is the buffer which serves to absorb losses. The smaller the buffer, the greater the risk that wrong decisions will lead to the downfall of the firm. Entrepreneurs therefore do not play the leverage effect to the hilt. The return of capital is more important than the return on capital.

The situation is very similar from the point of view of private and public households. An employee who takes on a lot of debt to buy a house ultimately speculates that his income will increase in the future, while the cost of borrowing remains fixed. In a natural monetary order, this may be true in some cases, but cannot be counted on. No one can be sure that the future course of events will be to their advantage. In addition, the leverage effect is a double-edged sword, because it can also be reversed: if the cost of borrowing is higher than the income generated by the production of goods, then it may not be the profits but the losses that are multiplied. For these reasons, the willingness to exploit leverage effects as much as possible is limited.

Fourth, under a natural monetary order, financial leverage effect limits itself. As the demand for credit grows, interest rates tend to rise, and thus the incentives for leverage are reduced and ultimately eliminated.

Fifth, under creeping price inflation, interest rates would rise quite soon even without any extensive use of the leverage effect. The reason is that a constantly rising price level means that creditors earn ever lower real returns. They therefore have an incentive to sidestep the credit market and use their savings elsewhere. But then there are only three options. Either they start investing in their own firms; or they buy durable consumer goods and real estate; or they no longer save at all, but start consuming their savings. In all three cases, the supply of loanable funds decreases and interest rates rise.

Sixth, with constantly rising price levels, there is an incentive for all market participants to look for alternative types of money. If there are suitable alternatives, then the demand for the bad money decreases, and it may even be completely forced out of the market for monies. Then the excessive debt economy will also come to an end.

Asset Markets Under Deliberate Price Inflation

The limits to price inflation that we have just highlighted exist only in a natural monetary order. In a modern system of compulsory dematerialized base money (fiat money), they are largely overridden, and thus there is a rampant, exponential growth of the asset markets.

A fiat-money system brings about permanent price inflation by its very nature—due to that what makes it different from a natural monetary order. The concrete persons, policies, and institutions involved in central banking are in this respect completely secondary, if not irrelevant, especially in the longer run. Natural money can only be produced at high cost and in comparatively small quantities. Fiat money can be produced in any quantity and in any time without any economic or technical limitations. The central banks of the Western world have proven this fact all too clearly in recent years.

The main purpose of a fiat money system is to increase the money stock. More specifically, it serves the purpose of increasing the money stock beyond the level it would have reached without government intervention. Otherwise it would be pointless to create such a system in the first place.

The basically unlimited possibility of inflating the money stock and the actualization of this possibility belong to the essence of fiat money. For this reason alone, the six limits discussed above are more relaxed here than in a natural monetary order.

Now we can imagine that the inflation of the money stock does not follow a fixed rule, but a random walk. Today, the money supply would grow by 5 percent, tomorrow by 70 percent, and the day after tomorrow by 12 percent. Today this person or firm, tomorrow another, would be in the front row when the new money comes onto the market, without it being possible to say in advance who the lucky winners of the inflation lottery will be. In this case, the rampant growth of asset markets would still be constrained in four ways (1) the risk of insolvency would increase as debt grows; (2) growing debt would lead to higher interest rates, because the supply of loanable funds does not necessarily develop in step with demand; (3) interest rates would also rise because price inflation leads to a reduction in the supply of loanable funds; and (4) the currency area would shrink due to currency competition.

However, the scenario of a purely random production of money is pure fiction. In the real economy, the inflation of the money stock follows a plan. There are specific people who decide on the inflation of the money stock, and there are specific people who stand to benefit from this inflation. One can argue whether this also belongs to the essence of a fiat money system; and one will probably have to affirm it, especially since the historical record is so crystal clear. Never ever has a fiat money system been introduced that works randomly. Always and everywhere, certain persons and groups are systematically favored.15 Indeed, what king, what prince, what democratic government would go through the trouble—and the dangers—of creating and maintaining a fiat money system without any possibility of steering and directing it?

But as soon as it is clear who is allowed to inflate the money stock, and in whose favor, two new consequences arise. On the one hand, the beneficiaries now have an incentive to rely on the central banks, to the detriment of all other money users (moral hazard). On the other hand, there is an incentive for all other market participants to join the circle of beneficiaries.

In a first step, let us assume that only those in charge of the fiat money system can directly benefit from the creation of money. Imagine the dictator of a banana republic who controls the printing press in such a way that only he himself or his relatives and friends are the direct beneficiaries, while everyone else has no access to this manna. (Later, we will drop this assumption and move closer to the actual conditions of the Western world.)

Then those who know that the money stock will be inflated in their favor can limit the risk-management resources to a symbolic minimum. The two essential tools of risk management in economic life are equity and liquidity. Enough cash on hand allows to make unforeseen payments without fire-selling any assets. Enough equity allows to absorb any losses. But these tools are costly. Money held in cash does not generate any income. A high equity base means renouncing the leverage effect. In short, increased security comes at the price of foregone returns.

However, he who can expect to be bailed out with the help of the printing press does not need to worry about managing risk. His cash reserves can be replenished at any time and without limit; and losses no longer pose a serious threat, because creditors can be serviced at any time and without limitation. So he can get into debt to his heart’s content in order to multiply his return on equity via leverage.

In addition, he does not need to exercise any special caution when investing capital. The potentially most profitable investments are usually also particularly risky and therefore costly; wherefore investors usually hold back here. But for the master of the printing press, costs do not matter. Because it is not he who bears the possible losses, but the entire community of money users. When the money stock is inflated in his favor, the value of each individual unit of money falls. In the case of risky investments, the possible profits therefore remain in his pocket, while the possible losses are largely borne by the other market participants. He therefore does not need to shy away from risks and will prefer particularly profitable investments.16

From his individual economic point of view, this behavior is not irrational. But it is obvious that a macroeconomic problem is now emerging. Our unleashed investor takes risks that he probably does not cover himself. He may incur costs that will ultimately have to be borne by the other market participants. Costs mean giving up scarce resources. The new money fresh out of the printing press is used to buy raw materials, labor, consumers’ goods, and so on, which are then necessarily lacking elsewhere. The exact location where this shortage will occur, however, cannot possibly be determined in advance. In principle, every household and every company can be affected, even if the respective activities are only financed with equity and without loans. The same applies to the timing.17 But in any case, the irresponsible actions of the master of the printing press create a contradiction between the planned use of resources on the one hand and the actually available resources on the other.18

Of course, planning errors also occur in a competitive economic order. And we should add that such errors are typically rectified without delay through the feedback mechanism of profits and losses. But this mechanism is hampered and delayed by the printing press. In the extreme case in which a central bank sets out to keep all firms in business with cheap credits out of nothing, a rectification can no longer result from firm-level losses. It will eventually have to be made on the level of the economy as a whole, in the context of a macroeconomic crisis. In other words, the feedback process between planning and reality is no longer decentralized and responsive even to minor discrepancies; rather, it now takes place on a macroeconomic scale and only after major imbalances have developed. The inflation of the money stock, the mere possibility of an (unlimited) inflation of the money stock sets in motion an illusory expansion of activities, which is finally corrected in a crisis.19

In the upswing, there is rampant growth in the asset markets. Most of the barriers that limit this growth in a natural monetary order are now suspended. The money supply can be increased indefinitely; there is no risk of insolvency for the masters of the printing press; and the latter do not have to fear an increase in interest, because all the necessary loans can be granted to them free of charge and for an unlimited period of time if necessary. Therefore, the rampant growth during the upswing can even be exponential.

However, two barriers remain, namely that resulting from price inflation and that resulting from the possible use of alternative types of money. As discussed above, price inflation tends to lead to a reduction in the supply of loanable funds. This may then result in the necessity for the masters of the printing press to compensate for those funds which they can no longer obtain at acceptable prices on the credit market by an even greater production of money. However, this is a double-edged sword. The increased inflation of the money stock accelerates the decline in the value of money and thus leads to a further reduction in the supply of loanable funds.20 Rising prices also entail sky-rocketing government spending and therefore the necessity to take on new and ever larger loans, which it then repays again by producing money, etc., etc. Eventually, prices rise so quickly that the money becomes unusable. If prices double from one day to the next—or even from morning to evening—then hardly anyone will want to hold this money. In extreme cases, this can lead to the currency being completely rejected by the citizens—it collapses and with it the entire division of labor.21

In the long run, all fiat money systems lead to this vicious cycle of inflation and price inflation. From there, three outcomes are possible. The first one is hyperinflation, followed by the crisis-like collapse of the fiat money system. Already during hyperinflation, citizens usually start to use foreign monies money and also natural types of money such as silver and gold coins; and this cushions the eventual collapse somewhat.

The second possible outcome is the decision of the masters of the printing press to stop the production of money or to reduce it to a minimum. In this case, an adjustment crisis is inevitable, but with two variants. Either the adjustment can be carried out by market forces, i.e. by a deflationary spiral; or the adjustment takes place through administrative fiat in a so-called currency reform.

The third possible outcome is to overwhelm the economy with price controls and other regulations to such an extent that free trade and exchange is no longer possible. In this way, too, (as in the case of the currency reform), the upcoming costs can be distributed to certain groups in a targeted manner. In contrast to a currency reform, however, there is a permanent nationalization of the economy.

Now, it may be objected that considerations of this sort have very little to do with today’s reality. We have spoken of privileged “masters of the printing press” or dictators of a banana republic. In fact, we assumed that they were the sole beneficiaries of inflation. But in Western countries today, such as the US or Germany (or the Eurozone countries), there is no one who could act in the monetary system in the manner of a landlord. Today, we have public central banks run by educated and well-meaning people. They act independently of the state and by no means take care only of a small circle of beneficiaries, but of more or less all market participants. They are bound by more or less strict rules. They have the mandate of stabilizing prices. This does not leave much room for arbitrary increases in the money stock.

This objection is somewhat justified. Present-day fiat money systems do indeed work somewhat differently than the rather primitive, hypothetical system we have examined so far. But the differences are ultimately differences of degree and, above all, they are unflattering for today’s reality. The primitive system adopted so far is characterized by the fact that the inflation benefits only the small stratum of the controllers of the system, while the vast majority have no prospect of penetrating this privileged circle. In contrast, in our current monetary system, practically all market participants can hope to join the ranks of the inflation winners, at least for a short time.22 As we shall show below, those circumstances exacerbate the adverse effects of fiat money.

Destabilizing Stabilization Policy

The core mission of monetary policy today is to stabilize the price inflation rate. The Eurosystem has no higher priority objective at all. All of its activities are supposed to be geared toward an annual price-inflation rate of around 2 percent. The US central bank system pursues a so-called dual mandate: stabilizing the price inflation rate and, if necessary, expanding monetary policy to stimulate the labor market (and, as a consequence of these two, to thereby achieve moderate long-term interest rates). Such stabilization policies are expected to have a positive effect on long-term growth. But the truth is that this stabilization is of a rather superficial sort and that it actually destabilizes the economy. Let us see why.

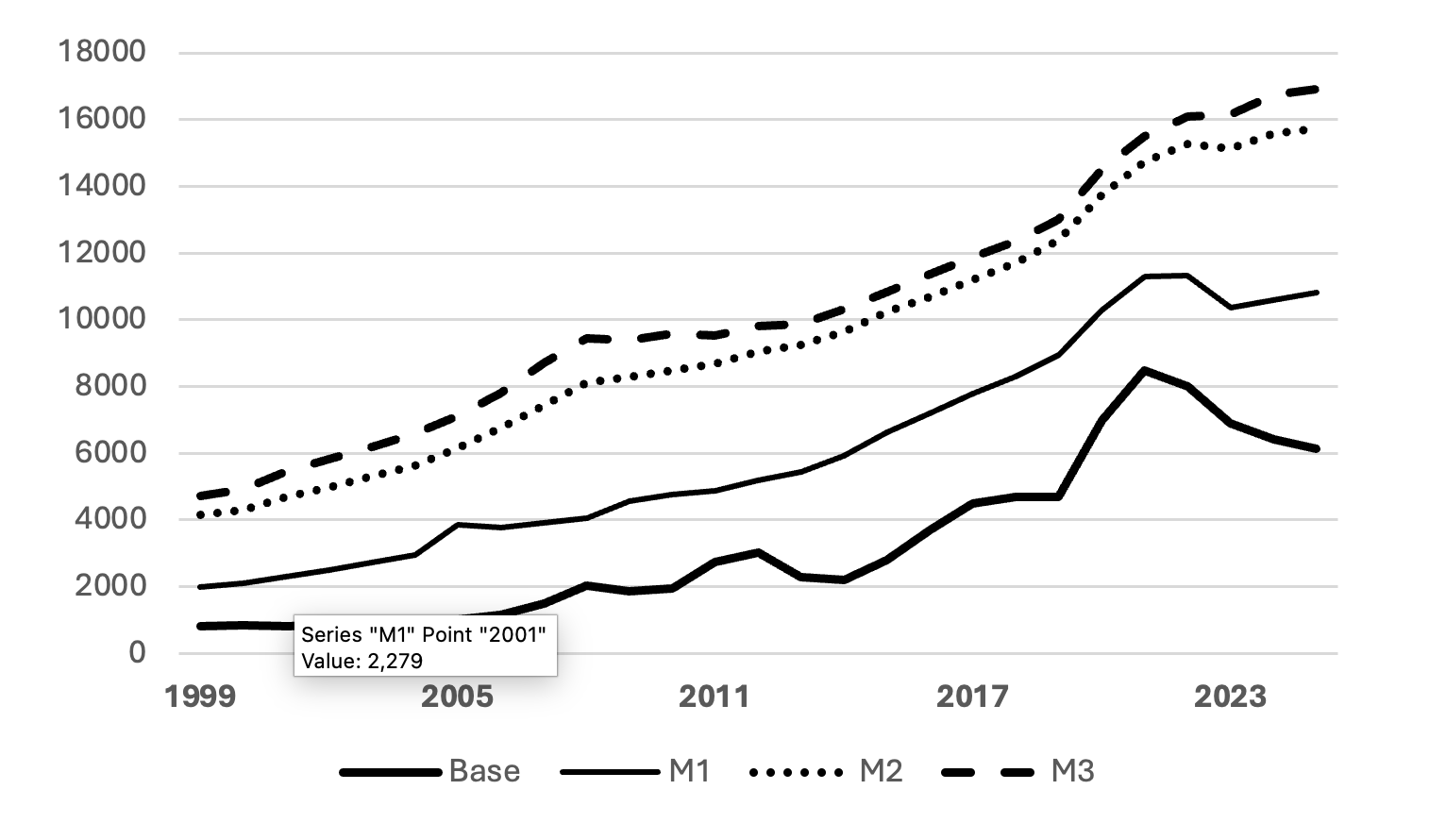

While in the fiat money system of a banana republic only the dictator is financed out of the printing press, today a much larger circle of market participants can count on the manna of ex nihilo money creation. This circle includes first and foremost the commercial banks. The most important reason is that the stabilization of the price inflation rate can only be achieved by stabilizing the entire money stock. However, most of the money supply is usually produced not by the central banks at all, but by the commercial banks (see Figure 3, below).

Figure 3

Monetary aggregates in the Euro area, 1999-2025

Source: ECB; Billions of euros

In order to stabilize the price inflation rate, central banks must ensure that commercial banks do not produce too much bank money; this may be done by making refinancing conditions more difficult (interest rate, maturity, collateral) and also by financial market regulation. On the other hand, however, they must also ensure that commercial banks do not produce too little bank money. To this end, refinancing conditions can be relaxed, but this is not always enough. Commercial banks can only produce bank money if they are solvent and liquid. But what happens if this is not the case?

It depends on how big and how networked the bank in question is. The smaller it is and the more limited its sphere of influence, the less impact its financial health has on the overall system. Payment defaults and insolvencies can therefore be tolerated by small banks. This is where the usual market process can do its work. But the situation is quite different for large banks that maintain business relationships with many other market participants. If a large bank has to sell securities under pressure, this puts pressure on market prices and therefore also on the balance sheet values of other banks holding the same type of securities. An initial liquidity problem can thus quickly develop into an insolvency problem, especially if the banks’ equity capital buffer is low. If a large bank defaults, then on the one hand this causes a significant slump in the total money supply; and on the other hand, there is a risk that the creditors will also be drawn into the insolvency vortex. Other commercial banks are among the most important creditors of commercial banks. The insolvency of a larger bank can easily lead to the insolvency of others.23

This is why central banks seek to prevent liquidity and solvency problems in the commercial banking sector. Of course, the provision of cash does not occasion any particular difficulties, because central banks can produce money at no cost. Things are somewhat different with the impending insolvency of a larger commercial bank. Additional liquidity is of no use here if this liquidity comes in the form of a loan, because then the liabilities would rise along with the assets and the insolvency would persist.

There are actually only three measures that help in the event of insolvency: first, the contribution of equity capital by the state; second, state permission to keep fictitious accounts; and thirdly, the creation of artificial markets for the assets of the bank concerned. All three techniques were used massively in the rescue of the banks in 2008 and 2009.24 However, the first two do not fall within the remit of central banks, so we will focus here on the third.

Central banks can prevent the insolvency of commercial banks by preventing the decline in the value of the assets held by the institutions concerned. These assets are mainly debt securities, and in some cases also shares. Central banks must therefore either buy these assets at artificially high prices, or accept them as collateral at artificially high values, or exchange them for their own assets at an artificially high exchange rate. This is exactly what has happened massively after the 2008 crisis and is still happening.

Many economists—especially in German-speaking countries—believe that stabilizing the financial markets is not one of the tasks of central banks. They are wrong. The stabilization of the financial markets is a more or less direct consequence of the core monetary policy task of today’s central banks, namely the stabilization of the rate of price inflation. To fulfill their mission, central banks must avoid the collapse of commercial banks at all costs; but sometimes they can only achieve this by preventing a collapse of the securities market. This concerns especially debt securities and, above all, sovereign debt.

Banks therefore have reason to invest their money in the securities of bad (but important) debtors, because they can assume that the prices of these securities will be supported by the central banks. Other government interventions are also working in the same direction, in particular the deposit insurance of demand (sight) deposits. The costs of these interventions are passed on to the general public—as in the above case of the banana republic—namely to the community of money users. Every time the central banks open the money floodgates to support this or that bank, or this or that security, the relative scarcity of money decreases. The beneficiaries of these interventions fill their coffers with fresh money, but the other holders of money are ultimately robbed of the its purchasing power, which in a natural monetary order preserves its relative scarcity and thus its purchasing power.

In our current fiat system, there is a massive incentive for the larger commercial banks to act accordingly. They know that central banks want to stabilize the rate of price inflation. They know that the central banks have unlimited resources at their disposal for this. They know that their own well-being is essential for central banks to achieve their public mission.25 Accordingly, commercial banks can cut back on their own (costly) risk management and devote a greater part of their resources to particularly risky (and therefore lucrative) investments. They can take on more debt and reduce their cash holdings in order to increase their return on equity through leverage. And that is exactly what they do.

The standard metric for measuring the financial leverage of commercial banks is the so-called CET1 ratio – the common equity tier 1 ratio. According to the IMF, the world-wide average CET1 ratio was 13 percent in 2024, based on a sample of 669 banks from 69 countries representing 74 percent of the global assets of the banking sector.26 An average CET1 ratio of 13 percent means banks hold debt securities worth 770 percent of their equity capital. But even this figure does not adequately represent the real situation. For the CET1 ratio is calculated by dividing the equity capital of banks, not by their assets, by their risk-weighted assets. Now the official risk weight of sovereign debt (treasury bills, government bonds, and similar), as defined in all international agreements between financial regulators, is exactly zero percent. This means that sovereign debt does not count at all for the calculation of the CET1 ratio. By holding significant amounts of sovereign debt, a commercial bank can therefore bring down its CET1 ratio, even though it is leveraged to the hilt and has made very risky investments.

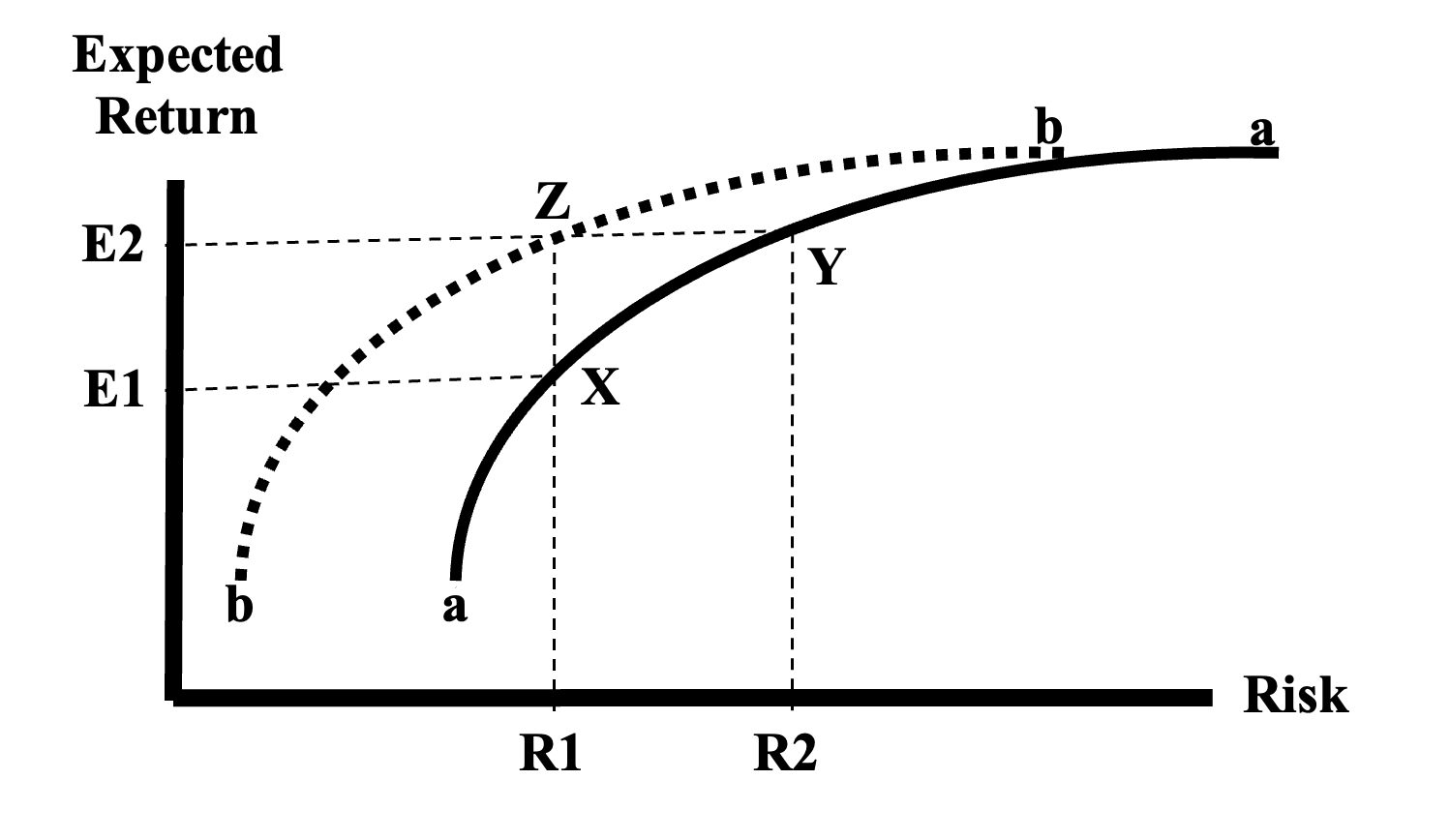

Figure 4

The impact of price-inflation rate stabilization on investment decisions

Let us give a graphical representation of this mechanism. The above Figure 4 shows an efficient frontier curve (a–a) illustrating the investment opportunities in a natural monetary order. The curve shows that an agent may achieve growing expected returns only by accepting ever higher risks (in the sense of possible consequences that are undesirable from his own point of view). Investment project Y promises a higher expected return (E2) than project X (E1), but is also associated with greater risks (R2 instead of R1). If our investor is relatively risk-averse, he will prefer X. However, he will reconsider this choice in a fiat money system. Because in this case, he does not bear all the risks. Some of the risks or costs are forcibly socialized. In his view, this means a shift in the efficient frontier from (a–a) to (b–b). Project Y now has the same level of risk (R1) as project X before in a natural monetary order. Our investor can therefore reconcile the relatively lower risk (R1) with the relatively higher expected return (E2) (point Z). He will therefore prefer the riskier investment project. From a macroeconomic point of view, therefore, greater risks are taken (more resources are consumed), while from an individual economic point of view, a better result is achieved with the same risk.27

It is obvious that the financial markets are structurally weakened as a result. Where the capital base is as thin as that of most commercial banks and other financial market participants, any major default entails domino effects that can drag the overall market with it, as it almost happened in the Fall of 2008. At that time, only the massive intervention of the central banks slowed down the implosion of the stock markets and stopped the disintegration of the commercial banks. But it follows, of course, that the latter found even greater encouragement.

At the macroeconomic level, the consequences are exactly the same as in the case of the “primitive” dictator in the previous section. The main difference to that case is that the reduction of individual risk provisions is now accelerated. The dictator of a banana republic can take his time, because no one can take away his advantages. Today’s commercial banks, on the other hand, are competing for market share and new shareholders, so they will hurry to exploit the leverage effect of debt as quickly as possible and as far as possible. While in the banana republic usually only the dictator (and his circle of friends) is heavily indebted, while the bulk of the population is constrained to relatively conservative financial behavior, in our progressive system whole armies indulge in the manna of credit expansion.

In today’s financial systems, commercial banks are only the first and immediate beneficiaries of the printing press.28 Indirectly, insurance companies, pension funds and all security holders in general also enjoy the individual economic advantages resulting from the stabilization of the most important securities prices. Indirectly, all bank customers can also enjoy the printing press. These include in particular the states and public budgets, but also companies in the financial sector, non-financial companies and households. As we have seen, with constant price inflation, there are strong economic incentives for every citizen to take the winning side of government-sponsored monetary policy. The easiest way to do this is through debt. Additional debt allows us to buy real estate and securities now, goods whose prices are likely to rise sooner or later as a result of the relentless production of money. The result is an inflation of the asset markets, which results not least from household debt.

| USA

(II/2024) |

UK

(2021) |

Eurozone

(2024) |

Japan

(2022) |

|||||

| Bn$ | % | Bn£ | % | B€ | % | Tr¥ | % | |

| GDP | 29.017 | 100 | 2.285 | 100 | 14.970 | 100 | 552 | 100 |

| All assets | 184.526 | 636 | 13.759 | 602 | 72.831 | 487 | 3.236 | 586 |

| Non-financial assets |

61.288 | 211 | 7.088 | 310 | 42.353 | 283 | 1.205 | 218 |

| Financial assets |

123.238 | 425 | 6.671 | 292 | 30.478 | 204 | 2.030 | 368 |

| Financial obligations | 20.729 | 71 | 2.139 | 94 | 8.875 | 59 | 381 | 69 |

Table

Household assets and debt relative to GDP

Sources: Federal Reserve, ONS, ECB, Cabinet Office; own calculation

The above table shows the current situation in a few selected countries. In the UK, private household debt is particularly high (the monetary value of its debt is 94 percent of GDP), while in the Eurozone it is somewhat more moderate (barely two-thirds of GDP). Also notice that the total value of assets in all four countries is many times the monetary value of annual production. Of course, this is fundamentally due to the fact that assets are accumulated—in wealthy countries, it is normal for their value to far exceed that of annual production. But the influence of the speculative overvaluation of assets—which takes different forms in different countries—also comes to light here.

It is common today for young families to go into debt to the extreme in order to buy the largest possible houses as early as possible.29 People with an entrepreneurial streak often come up with the idea of “collecting” rental apartments, which they finance through ever new loans, each of which is secured with the property in question. Even households with a very moderate income from their main occupation can buy a credit-financed real estate park in this way. This behavior is perfectly rational from an individual economic point of view. In a price-inflationary environment, it is justified to expect a sustainable increase in the value of the property. Debt service, on the other hand, does not increase, at least not when the interest rate is fixed. So the possible revenues are open to the top, while the costs are limited. The profits are private, the costs at least partially socialized.

From a macroeconomic point of view, this results in growing financial fragility that extends far beyond the financial sector. A debt economy is vulnerable because the bankruptcy of individual over-indebted market participants entails the bankruptcy of their creditors if they are also over-indebted. This then leads to an avalanche-like wave of bankruptcies that affects more or less all parts of the economy.

With a low level of debt or a high equity base of the economy as a whole, isolated bankruptcies do not make any big waves. Their negative effects are usually limited to the immediate environment (family, friends, employers, employees, customers, suppliers) of the debtor in question. The equity in this environment has an error-absorbing effect. It breaks the wave of bankruptcies or prevents such a wave from occurring in the first place. It is different in a fully developed debt economy, as it is produced by a fiat money system. Here, bankruptcies can make very big waves. For when the creditors themselves have high debts, they transfer and multiply the original bankruptcy of their own debtors. Lack of equity in the context of bankruptcy promotes or intensifies waves of bankruptcies.

Of course, such waves of bankruptcies are all the more important the larger the debtor in question. Today, some banks and insurance companies are so large that their eventual bankruptcy would practically drag the global financial industry into the abyss. The same applies to the largest industrial companies. Their bankruptcy would also result in that of their creditors and spread from there in all the stronger waves to the rest of the economy. Companies that are large enough to unleash such an avalanche are called “systemically important” in contemporary jargon. However, it should be noted that the systemically relevant quantity is not a natural constant. Rather, it depends in particular on the level of indebtedness of the financial sector as a whole. The more banks and insurance companies get into debt, the more susceptible they become to the bankruptcies of smaller and smaller market participants.

In other words, the greater the level of debt within an economic order, the more susceptible the whole becomes to the misconduct of smaller and smaller parts. If it were possible to take the of debt of our day to its theoretical peak; if it were possible to indebted every single company (not only in the financial sector) and every single household (not only the public budgets) to a similar extent as we have so far only known from the banking and insurance sector; then even the smallest company and even the smallest household would be systemically relevant. The bankruptcy of one plumber or bakery could then lead to the bankruptcy of all other companies and households.30

Some ingenious theorists have used the image of a butterfly to illustrate this situation, whose gentle wing beats can have enormous effects. Imagine: The sight of a butterfly suddenly appearing awakens the love of God of a plumber who is heavily in debt. From one moment to the next, he decides to leave his work and continue his life as a monk. He goes bankrupt, his company is liquidated, and he also loses his private assets. It means nothing to him anymore. But his bank now has a problem. It has made provisions to the best of its knowledge and belief, has built up provisions and taken out insurance policies in order to be prepared for all possible cases of payment defaults. But it did not foresee this case. The butterfly was not on its bill. Now it is going bankrupt for its part, the avalanche set off by the plumber is intensified, and in a short time all other market participants are bankrupt.

One crucial point must be emphasized again and again: There is no natural tendency towards a debt economy. On the contrary, there are usually good reasons for all parties involved to avoid debt as much as possible. However, the stabilization policy of the central banks leads to a economy-wide high level of debt, which in turn is only possible under a fiat money system. Butterflies usually have no significant impact on economic life. However, the policy of stabilizing the value of money tends to lead to the fact that butterflies could also become a source of danger for the economy as a whole at some point.

Monetary Stabilization and Market Socialism

Let us summarize the foregoing considerations. Stabilization policies by modern central banks do not put the printing press at the service of the common good. That may be the intention of the executives, but the reality is different. Stabilization policies have led to the largest debt and the largest inflation of the securities and real estate markets of all time; and this was no accidental mishap. Price-inflation targeting (and all similar policies) socializes the short-term inflation gains. This distinguishes it from the supposedly primitive use of the printing press in banana republics. But this socialization means that the problems that would only afflict the dictator and his circle in a banana republic are now generalizing.

The monetary socialism of our day is well known to the economists of the Austrian School. But even the Austrians have typically seen it only in the fact that a central state institution—the central bank—is entrusted with the production of the general medium of exchange; and that this centrally planned economy thus suffers from the usual problems of central planning.31 But as we have seen, monetary socialism gives birth to a whole series of socialist children from his womb. It produces a very special kind of socialism in the asset markets.

This kind of socialism was known to the theorists of the 1920s and 1930s, but since then it has disappeared from the limelight because it seemed to be completely irrelevant in practice. Today, however, it is omnipresent, only it sails under a false flag. It is called predatory capitalism, turbo-capitalism and other false names. Before the WWII, it was known as “market socialism.” Some socialist theorists at the time wanted to combine the advantages of the market with those of socialism. They proposed that the heads of the socialist enterprises be granted extensive powers in order to exploit the advantages of decentralized decision-making. Ludwig von Mises pointed out as early as 1922 the central flaw of this idea:

But the problem is not nearly so much the question of the manager’s share in the profit, as of his share in the losses which arise through his conduct of business. […] To make a man materially interested in profits and hardly concerned in losses simply encourages a lack of seriousness. This is the experience, not only of public undertakings but also of all private enterprises, which have granted to comparatively poor employees in managerial posts rights to a percentage of the profits.32

Eighteen years later, he became even more explicit:

If the socialist economy were to place the control of capital in the hands of quasi-speculators, it would turn them into irresponsible masters of the economy. No one who wants to be taken seriously could make or advocate such an absurd proposal. A socialist economy that set out to regulate the use of capital in this way would no longer be a socialist and planned economy; nor would it be capitalist. It would be chaotic.33

Meanwhile, the chaos has arrived. Our times witness an unprecedented inflation of the asset markets, propelled by public policies that ostensibly serve to stabilize the value of money. The commanding heights of our irresponsible masters are a huge pile of debt. Day-in day-out, the central banks inflate that pile ever further.

There is only one thing Mises did not quite foresee: that this absurd system would one day be considered to be the epitome of capitalism and would even be defended by many economists.

- Jörg Guido Hülsmann ([email protected]) is Professor of Economics at the Faculty of Law, Economics, and Management of the University of Angers, France; a Senior Fellow with the Ludwig von Mises Institute; and the author of Mises: The Last Knight of Liberalism (2007), The Ethics of Money Production (2008), and Abundance, Generosity, and the State (2024). [↩]

- See Vytautas Zukauskas and Jörg Guido Hülsmann, “Financial Asset Valuations: The Total Demand Approach,” Quarterly Review of Economics and Finance 72 (May 2019): 121–131. [↩]

- See Philipp Bagus, “Asset Prices—An Austrian Perspective,” Procesos de Mercado IV, no. 2 (Oct. 2007): 57–93; Brendan Brown, “A Modern Concept of Asset Price Inflation in Boom and Depression,” Q.J. Austrian Econ. 20, no. 1 (Spring 2017): 29–60; Zukauskas and Hülsmann, “Financial Asset Valuations: The Total Demand Approach.” [↩]

- See Ludwig von Mises, Theorie des Geldes und der Umlaufsmittel (Munich: Duncker & Humblot, 1912), p. 318; idem, The Theory of Money and Credit (Auburn, Ala.: Mises Institute, 2009 [1953]), p. 218. [↩]

- The sovereign-debt crisis of the early 2010s had led to a revival of the discussion about the pros and cons of money creation by donation. In the United States, a proposal was made at the end of 2012 that the Treasury Department should simply mint a platinum coin with a face value of one trillion dollars, which could then be redeemed at the central bank for the corresponding amount. See, e.g., Eric Morath, “‘Joke’ Solution to Debt Clash Gets Serious Study,” Wall Street Journal (Jan. 7, 2013). In France, presidential candidate Marine Le Pen recommended that the Banque de France be removed from the Eurosystem and completely nationalized in order to enable it to finance government spending directly from the printing press. See Mathias Thépot, “Financement du déficit : mais où va Marine Le Pen ?”, La Tribune (Feb. 8, 2017); “Marine Le Pen lève le voile sur son programme, pas sur son financement,” Ouest-France (Feb. 4, 2017). [↩]

- One could object that, even today, any sum of money created out of thin air is at least partially given away. After all, the additional loans can only find buyers if they are lent on better terms. Thus, when central banks create money and lend that new money, they necessarily undercut the credit terms—interest rate, collateral, maturity, etc.—that would prevail without their intervention. But even this gift component does not change the principle of credit-based money creation. The first users of the new sums of money will have to repay the corresponding amounts sooner or later, and they will also have to pay interest on the amount borrowed. In other words, these are not pure gifts, but loans with a gift component. [↩]

- See Thibaut Picard and Dilyara Salakhova, “Secured and Unsecured Interbank Markets: Monetary Policy, Substitution and the Cost of Collateral” (Banque de France WP no. 730, September 2019), especially pp. 6-9. Nikolay Gertchev has brilliantly explained how the interbank market of the early 2010s evaporated under the impact of heavy handed central-bank interventions. See Nikolay Gertchev, “The Inter-Bank Market in the Perspective of Fractional Reserve Banking,” in Theory of Money and Fiduciary Media, Jörg Guido Hülsmann, ed. (Auburn, Ala.: Mises Institute, 2012). [↩]

- This immobility may can also turn out to be a disadvantage. Real estate does not allow to side-step or evade high taxation, whereas movable assets may be held abroad. [↩]

- We will come back to the special case of precious metals—especially gold—separately later. [↩]

- On the concept of a natural (or free-market) monetary order (as compared to interventionist monetary systems) see Hülsmann, The Ethics of Money Production, op. cit., chap. 14. [↩]

- Many economists and financial theorists understand the risk of an investment as the statistical probability that the return will deviate (standard deviation) from some value regarded as normal. This approach suffers from numerous theoretical and practical difficulties, not least the problem of determining what constitutes such a “normal” value. I therefore prefer a different, broader definition of risk, namely, the probability that an undesirable event (undesirable from the point of view of the acting person) will occur in the future. In regard to probability theory, I rely on the realist approach developed by Ludwig von Mises, Human Action: A Treatise on Economics, Scholar’s ed. (Auburn, Ala: Mises Institute, 1998), ch. VI. [↩]

- The economics of the “reservation demand” (or “demand to hold” on the part of the current owners) goes back to Philip Wicksteed and has been developed by by Murray N. Rothbard, Man, Economy, and State, with Power and Market, Scholar’s ed., 2nd ed. (Auburn, Ala.: Mises Institute, 2009), Man, Economy, and State, ch. 2, §8. [↩]

- See Jörg Guido Hülsmann, “Fiat Money and the Distribution of Incomes and Wealth,” in David Howden and Joseph T. Salerno, eds., The Fed at One Hundred—A Critical View on the Federal Reserve System (Berlin: Springer, 2014), pp. 127-138. [↩]

- However, this is only true as long as price inflation is relatively weak. When inflation is high, savers are easily discouraged and decide to consume their income and financial assets right away. This then means a reduction in the supply side of the banking industry. [↩]

- Murray Rothbard revelled (and excelled) in naming names when it came to the beneficiaries of government interventionism, and especially monetary interventionism. See for example Murray N. Rothbard, A History of Money and Banking in the United States (Auburn, Ala.: Mises Institute, 2002); ibid., Conceived in Liberty, vol. II (1999 [1975]): “Salutary Neglect”: The American Colonies in the First Half of the Eighteenth Century (Auburn, Ala.: Mises Institute), chap. 26; vol. III (1999 [1976]): Advance to Revolution, 1760-1775 (Auburn, Ala.: Mises Institute), chaps 6, 7, 19, 35; vol. IV (1999 [1979]): The Revolutionary War, 1775-1784 (Auburn, Ala.: Mises Institute), chaps 10, 67–70. [↩]

- The same applies to high-risk trading strategies such as maturity transformation or the so-called carry trade (debt in one currency, investment in another). On the influence of monetary policy interventions on maturity transformation, see Philipp Bagus, “Austrian Business Cycle Theory: Are 100 Percent Reserves Sufficient to Prevent a Business Cycle?”, Libertarian Papers 2, Art. 2 (2010); and Philipp Bagus and David Howden, “The Term Structure of Savings, the Yield Curve, and Maturity Mismatching,” Q. J. Austrian Econ. 13, no. 3 (Fall 2010): 64–85. [↩]

- In other words, the likelihood of that event has nothing to do with the particular circumstances arising from the activities of the operator concerned (i.e., case probability). Rather, this probability is defined by the economic system as a whole. Individual market participants are equally likely to become victims (class probability). A more detailed discussion of this distinction can be found in Mises, Human Action, ch. VI, §3–4; see also Hans-Hermann Hoppe, “The Limits of Numerical Probability: Frank H. Knight and Ludwig von Mises and the Frequency of Interpretation,” “The Yield from Money Held” Reconsidered,” and “On Certainty and Uncertainty, Or: How Rational Can Our Expectations Be?”, all in The Great Fiction: Property, Economy, Society, and the Politics of Decline, 2nd ed (Auburn, Ala.: Mises Institute, 2021). [↩]

- Mathematically speaking, what we have here is a nonlinear process. It is possible for everything to go well for a long time, with the risks taken not leading to actual costs. But the pitcher goes to the well only until it breaks. Eventually it will come to the point at which the overstraining of the available resources occurs which had previously been only latent. [↩]

- According to the traditional Misesian crisis theory, intertemporal imbalances in the structure of production occur when monetary interventions entail artificially low interest rates. However, the above considerations lead to the conclusion that monetary interventions may lead to imbalances and crises even without any reduction of the interest rate. Cf. Jörg Guido Hülsmann, “Toward a General Theory of Error Cycles,” Q.J. Austrian Econ. 1, no. 4 (Winter 1998): 1–23, esp. p. 20; Roger W. Garrison, Time and Money: The Macroeconomics of Capital Structure (London and New York: Routledge, 2001), p. 112ff. Robert C.B. Miller has taken up this idea and developed it further. However, he narrows the problem, since in his opinion it only occurs when interest rates are also artificially lowered. Cf. Robert C.B. Miller, “Systemic Appraisal Optimism and Austrian Business Cycle Theory,” Q.J. Austrian Econ. 15, no. 4 (Winder 2012): 432–442. Similar considerations were also made by Tyler Cowen; cf. his work Risk and Business Cycles: New and Old Austrian Perspectives (London and New York: Routledge, 1997). [↩]

- It was precisely this circumstance that caused great difficulties for the German commercial banks in the inflationary years 1914–1923 and led to an erosion of their equity base. Cf. Lothar Gall et al., Deutsche Bank, 1870-1995 (Munich: C.H. Beck, 1995), p. 222f; and the English translation, idem, The Deutsche Bank 1870–1995 (London: Weidenfeld & Nicolson, 1995). Proliferating credit markets only occur when price inflation is creeping, not galloping. [↩]

- As Peter Bernholz, emeritus professor of economics at the University of Basel, has meticulously demonstrated in several publications, all historical hyperinflations have arisen in this way. Government over-indebtedness in a fiat paper money system repeatedly made resorting to the printing press irresistible, and from this developed a fatal inflationary spiral. Cf. Peter Bernholz, Monetary Regimes and Inflation: History, Economic and Political Relationships, 2nd ed. (Cheltenham, UK and Northampton, MA: Edward Elgar Publishing, 2015). [↩]

- We see here a structural analogy between modern monetary (banking) systems and modern political (republican) systems. See George Bragues, Money, Markets, and Democracy: Politically Skewed Financial Markets and How to Fix Them (New York: Palgrave, 2016). Hans-Hermann Hoppe points out that in democracy, “Everyone—not just the hereditary class of nobles—is permitted to become a government official and exercise every government function. … Rather than being restricted to princes and nobles, privilege, protectionism, and legal discrimination will be available to all and can be exercised by everyone.” Hans-Hermann Hoppe, “On the Errors of Classical Liberalism and the Future of Liberty,” pp. 232–233, in Democracy: The God That Failed (Transaction, 2001); see also idem, “On Monarchy, Democracy, Public Opinion, and Delegitimation,” in same, pp. 82–83. [↩]

- On the contagion or domino effect of such an inherently insolvent system, whereby the collapse of one bank spreads to others in a type of chain reaction, see Jörg Guido Hülsmann, The Ethics of Money Production (Auburn, Ala.: Mises Institute, 2008), p. 143 et pass.; idem, “Has Fractional-Reserve Banking Really Passed the Market Test?”, The Independent Review VII, no. 3 (Winter 2003): 399–422, p. 407 et pass.; idem, “Free Banking and Fractional Reserves: Response to Pascal Salin,” Q.J. Austrian Econ. 1, no. 3 (Fall 1998): 67–71, pp. 69–70; and idem, “Free Banking and the Free Bankers,” Rev. Austrian Econ. 9, no. 1 (1996): 3–53, p. 36 et seq. [↩]

- The plans for this were devised and published a few years earlier. Cf. Ben S. Bernanke and Vincent R. Reinhart, “Conducting Monetary Policy at Very Low Short-Term Interest Rates,” American Economic Review 94, no. 2 (2004): 85–90. [↩]

- And we should add that the central banks know this, too. The moral hazard that today is so prevalent in the financial sector is not at all, as the standard neoclassical theory has it, a consequence of asymmetric information, but a consequence of the violation of property rights. See Jörg Guido Hülsmann “The Political Economy of Moral Hazard” Politická ekonomie, vol. 54, no. 1 (2006), pp. 35–47. [↩]

- See International Monetary Fund, Global Financial Stability Report: Shifting the Ground Beneath the Calm (Washington, DC: International Monetary Fund, October 2025), p. 21. [↩]

- In order to prevent misunderstandings, we would like to expressly point out at this point that we do not associate these statements with any accusations against bankers, fund managers and other financial market participants. As Charles Holt Carroll wrote more than a hundred and fifty years ago, the problem here concerns the economic order as a whole, not individual market participants. Cf. Charles Holt Carroll, Organization of Debt into Currency and Other Papers, reprint ed. (New York: Arno Press & The New York Times, 1972 [1964]), pp. 77, 94, 105 et pass. [↩]

- In the USA, the circle of immediate beneficiaries (the so-called primary dealers) count only some 20-30 (partly foreign) commercial banks. In the Eurosystem, the circle is much larger and includes several thousand commercial banks from the entire euro area. However, there are also certain transactions here to which only a smaller circle of about 100 high-turnover banks are admitted. [↩]

- It is somewhat more difficult for a private household to speculate in the same way on rising securities prices. The lenders (usually banks) would prefer to collateralize the sums they lend with real estate rather than securities. But at least those who have largely paid off their real estate loan can then go into debt again—this time to purchase securities or commodities. [↩]

- At the moment, this is not yet the case. Therefore, private individuals are not yet under the protection of the central banks. In the USA, a New York cleaning lady made headlines a few years ago. Over time, she had acquired apartments and houses worth more than a million dollars, of course financed with loans. The collapse of the real estate market in 2007–2008 then brought a temporary end to her dealings, without any intervention by the central bank. [↩]

- See for example Jesús Huerta de Soto, Money, Bank Credit and Economic Cycles, Melinda A. Stroup, trans., 4th ed. (Auburn, Ala.: Mises Institute, 2020), ch. 8, §3; Roland Baader, Money-Socialism: The Real Causes of the New Global Depression, Robert Grözinger, trans. (Gräfelfing: Verlag Johannes Müller, 2010). [↩]

- Ludwig von Mises, Socialism: An Economic and Sociological Analysis, J. Kahane, trans. (Indianapolis, Ind: Liberty Fund, 1981), ch. 11, §, p.186. See also idem, Human Action, ch. XXVI, §5, pp. 702–703, 706. Entrepreneurship means acting under uncertainty. This fundamental fact has been lost sight of by academic economics for decades and has only recently been addressed again. Cf. Peter G. Klein, “Risk, Uncertainty, and Economic Organization,” in Property, Freedom, and Society: Essays in Honor of Hans-Hermann Hoppe, Jörg Guido Hülsmann and Stephan Kinsella, eds. (Auburn, Ala.: Mises Institute, 2009). On why it is impossible for central economic planners to “play market,” see Mises, Socialism, ch. 6, §4, and idem, Human Action, pp. 707–708. [↩]

- Ludwig von Mises, Nationalökonomie: Theorie des Handelns und Wirtschaftens (Geneva: Éditions Union, 1940), p. 640 [translation JGH]. The corresponding text in Human Action (chap. XXVI, §5, pp. 705–706) reads as follows:

If the director were without hesitation to allocate the funds available to those who bid most, he would simply put a premium upon audacity, carelessness, and unreasonable optimism. He would abdicate in favor of the least scrupulous visionaries or scoundrels. He must reserve to himself the decision on how society’s funds should be utilized. But then we are back again where we started: the director, in his endeavors to direct production activities, is not aided by the division of intellectual labor which under capitalism provides a practicable method for economic calculation. [↩]

Follow Us!